guide

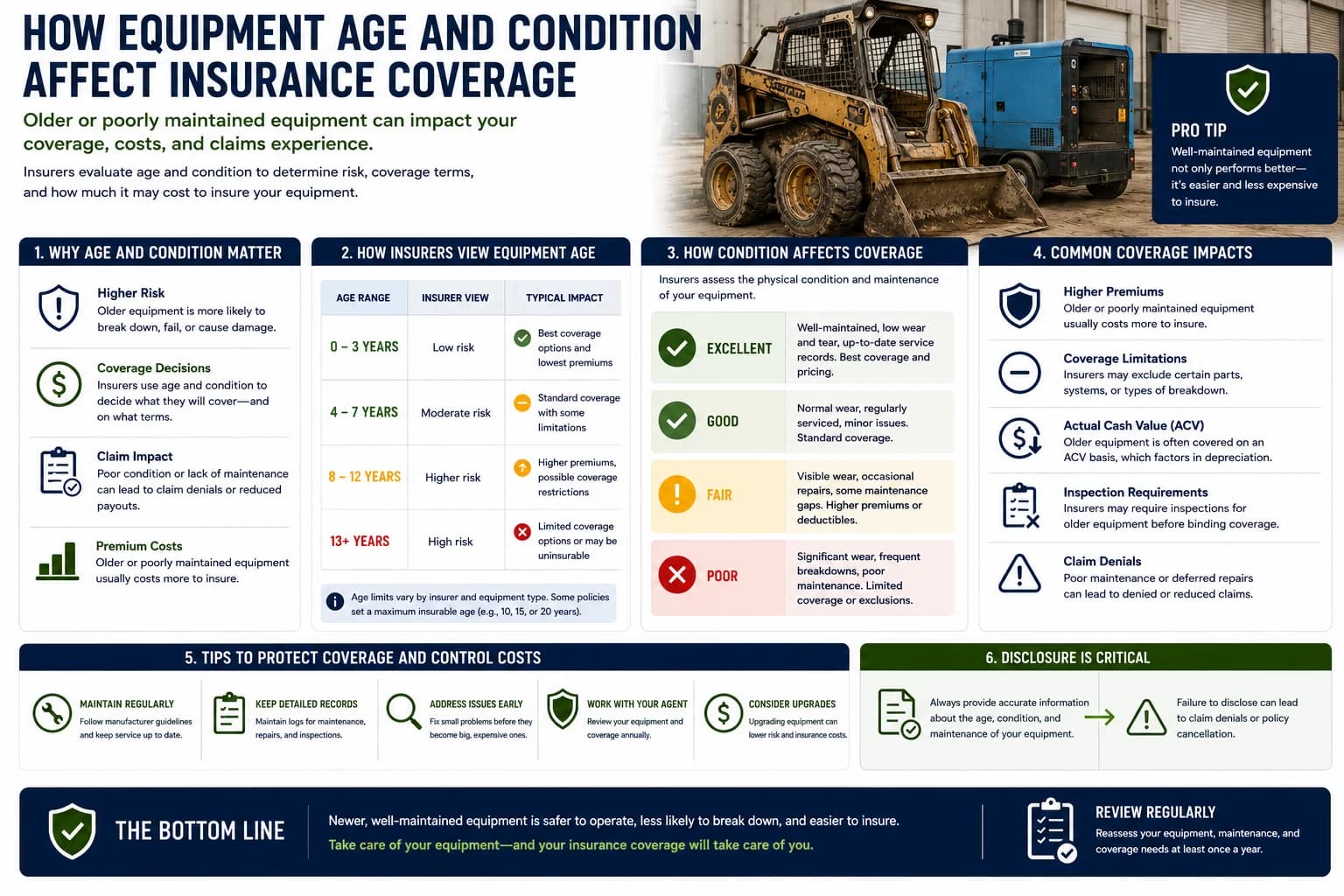

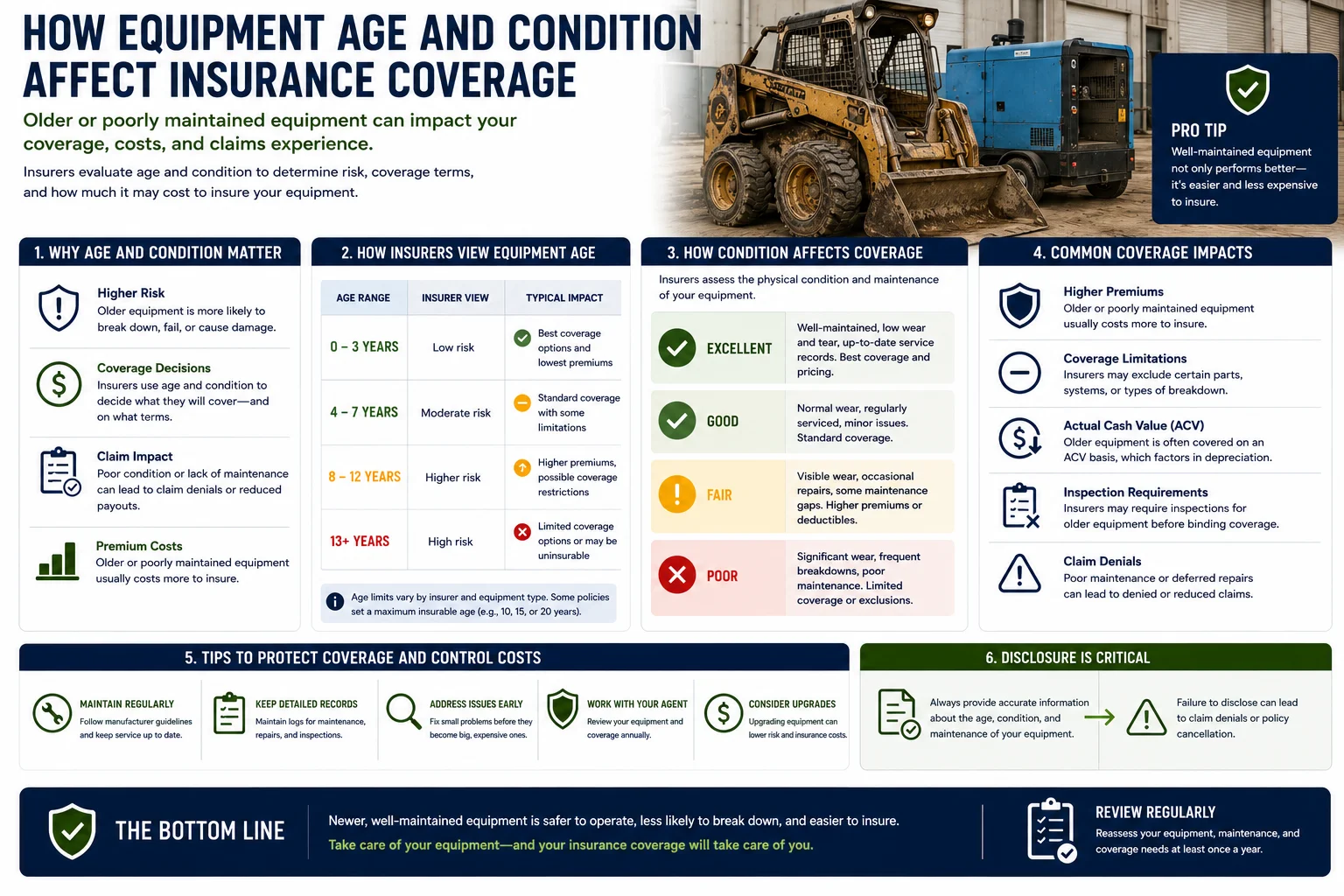

How Equipment Age and Condition Affect Insurance Coverage

Learn how equipment age, maintenance, condition, obsolescence, and valuation may influence underwriting, limits, premiums, and claim settlements.

{kind=link}

Introduction

Two pieces of equipment with the same model name can present very different insurance risks. One may be recently purchased, well maintained, and fully documented. The other may be older, heavily used, difficult to repair, and missing service records.

Equipment age and condition can influence how insurers evaluate risk, what valuation method applies, which inspections are required, and how a covered loss is settled.

This article provides general educational information. Insurance practices vary by insurer and policy. Consult a licensed insurance professional.

Why Age Matters

As equipment ages, it may become:

- More likely to fail

- More expensive to repair

- Harder to obtain parts for

- Less valuable in the resale market

- More technologically obsolete

Age alone does not determine insurability, but it can affect underwriting and valuation.

Why Condition Matters

Condition reflects how equipment has been used and maintained.

Insurers or appraisers may consider:

- Visible wear

- Corrosion

- Structural damage

- Leaks

- Safety-system condition

- Maintenance history

- Repair quality

- Operating environment

Well-maintained older equipment may present a better risk than neglected newer equipment.

Actual Cash Value and Depreciation

Older equipment is often more affected by actual-cash-value settlements.

Factors may include:

- Original cost

- Age

- Useful life

- Condition

- Market value

- Obsolescence

The amount needed to buy a replacement can be higher than the depreciated value of the damaged asset.

Replacement Cost Limitations

Replacement cost coverage may include conditions.

The policy may require:

- Actual replacement within a set period

- Comparable equipment

- Accurate declared values

- Compliance with policy reporting requirements

Some older equipment may be insured on a different basis if direct replacement is impractical.

Maintenance and Insurability

Insurers may ask about maintenance for high-value or specialized equipment.

Useful records include:

- Preventive maintenance schedules

- Service logs

- Inspection reports

- Repair invoices

- Technician findings

- Calibration records

- Rebuild documentation

These records help show that deterioration was managed rather than ignored.

Obsolete or Unsupported Equipment

Obsolete equipment can create special challenges.

Potential issues include:

- Discontinued parts

- Limited repair vendors

- Unsupported control systems

- Long downtime

- No direct replacement model

Businesses should discuss how the policy values equipment that cannot be replaced with an identical model.

Updating Insured Values

Equipment values can change because of:

- Inflation

- Supply shortages

- Major rebuilds

- Added attachments

- Market demand

- Technological obsolescence

Insurance schedules should be reviewed regularly rather than relying on the original purchase price forever.

Preparing Condition Records

Maintain:

- Current photos

- Serial number photos

- Meter readings

- Inspection results

- Service history

- Upgrade records

- Major repair invoices

- Current replacement estimates

Condition records are most useful when created before a loss.

Common Mistakes

Avoid:

Insuring at Original Cost Only

Original cost may not reflect current replacement cost or value.

Missing Maintenance Records

Undocumented service history can create uncertainty.

Ignoring Major Upgrades

Rebuilds and attachments may change value.

Leaving Retired Equipment Scheduled

Insurance records should match active assets.

Conclusion

Equipment age and condition can influence underwriting, valuation, and claim outcomes. Accurate maintenance records, current photos, and updated values help insurance professionals understand the asset more clearly.

Businesses should review older, rebuilt, or obsolete equipment individually and confirm how each asset would be valued after a covered loss.